Get Ready For Summer Volatility

July and August normally means school’s out and it’s time for fun in the sun.

To traders, it means get ready for summer volatility.

Face it: we’re mid-summer and most of us are focused on relaxing. And while the world is finally reopening from the pandemic, taking a relaxing break makes a lot of sense right now.

Kids go to camp and Wall Street traders tee up their mandatory 2-week vacations. And before traders check out, it’s normal for them to button up risk while they’re out. Their mindset is to flatten out their books and chill.

When traders drop stocks for rosé – fun in the sun means liquidity dries up. They say when the cat’s away the mice will play: with less traders trading, stocks get whippy. High-frequency traders and algorithms take advantage of lower liquidity to push stocks around. Volatility usually increases.

That’s precisely what we’ve come to expect for summer months.

A good friend always says that they should just close the markets in August and reopen in September. And for good reason: Typically, the summer months, especially August, are volatile.

History says to expect a bumpy patch near-term. Our data is starting to shift too. Until last week, bulls were in full force as buyers led the charge. But recently that tone has shifted.

Some of our indicators are suddenly telling us to get ready for summer volatility. But we should also have a plan. Short-term it will likely be bumpy. But, don’t get too bearish, because as I’ll show you, a green zone will come too.

That’s where the opportunity is.

So let’s first check in on our changing data.

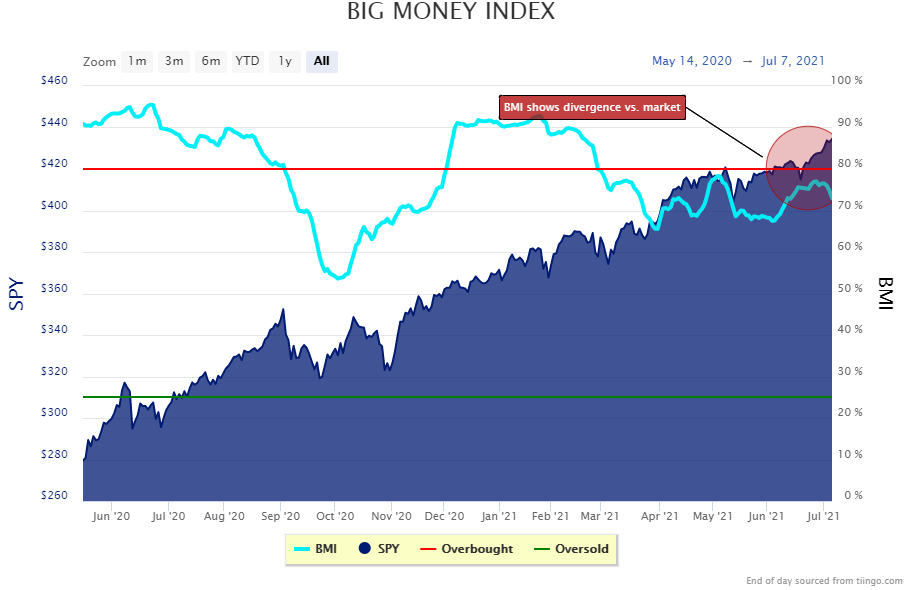

Big Money Index Get Ready For Summer Volatility

Up until this week, our data has been bullish. That means buyers were plentiful. But, suddenly that’s changing.

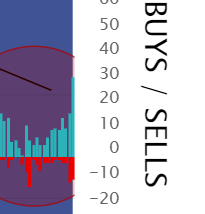

Tuesday and Wednesday saw a notable pick-up in selling, putting pressure on the Big Money Index:

Circled to the right, you can see a divergence happening in our data. Selling is increasing as the market makes new all-time highs. This points to weakening breadth while leadership is thinning.

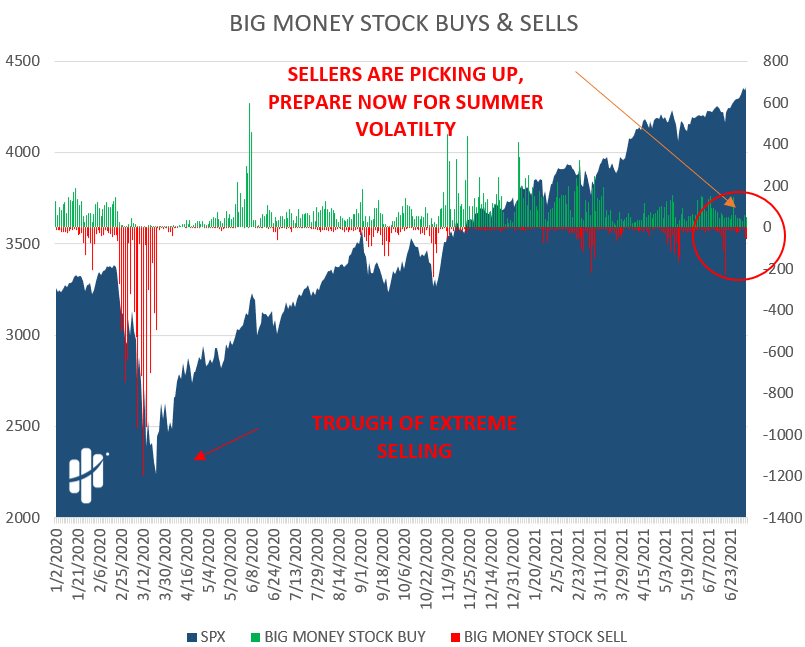

And you can see this same pattern under the surface of the BMI. The number of stocks firing sell signals is increasing:

Here’s a closer look:

You can see the obvious uptick in red over the last 2 days, but also notice the decline in green too. Those shorter green bars show less stocks getting bought compared to a few weeks ago.

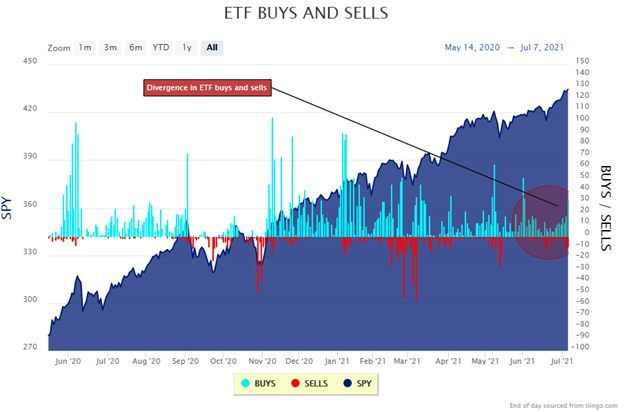

We notice the same type of action in ETFs too. Yesterday had quite a bit of buying, but also an uptick in selling. This divergence is also telling us to get ready for summer volatility:

Here’s a zoom-in:

ETFs that saw buying were bonds, technology, & healthcare. The ones getting sold were banks & Chinese stocks.

So, from a data standpoint, the message is to get ready for more rips and dips.

And history agrees.

July And August Are Historically Volatile Months For Stocks

It’s one thing when data suggests near-term pressure, it’s another altogether when history says to expect it too.

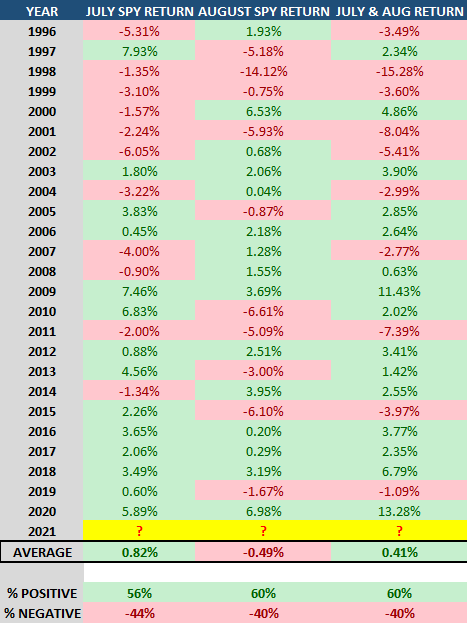

This morning I ran some numbers and found since 1996, the S&P 500 (SPY ETF) tends to produce mediocre results in July & August:

As seen above, July is a positive month a little better than half of the time, while August averages a negative expectancy. The two months together don’t look exciting with a market average of just +.41% return. This fits with our narrative to get ready for summer volatility.

But that’s only half the story. Remember earlier when I told you there’s a green zone coming?

What I also found in this study is what comes after the summer is JUICE.

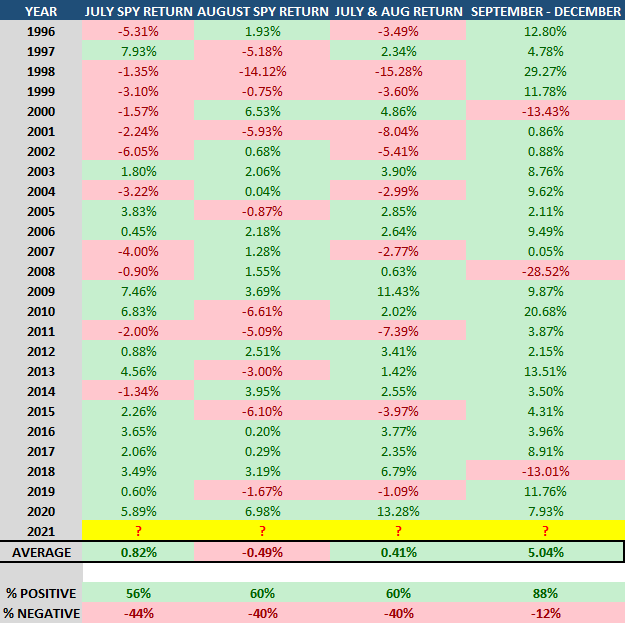

For the past 25 years, September – December is incredibly green:

Based on this table, history shows us that the 4 months of September – December have a historical average of just over 5%. That’s 11X greater than the +.41% expectancy of the combined July and August months. Obviously this isn’t an apples to apples comparison, but it does suggest something…

Heading into year-end usually means rocket launch time. That’s mega juice!

So, let’s tie this all together.

Here’s the bottom line: Stock and ETF selling is increasing, putting pressure on the Big Money Index. If the BMI falls further, we expect that stocks will follow. And history shows that July and August are lackluster for market returns.

Get ready for summer volatility. But also prepare for what comes next: July and August lead into a historically green time of year: September – December.

If you’re an active trader, consider trimming non-core positions.

If you’re like us, start making your outlier shopping list. Sometimes Christmas comes in July.