Macro Drivers Signal a Broadening Rally in 2024

Last year’s Tech-heavy rally was an either-or year. Essentially, the Tech bet worked much better than everything else.

This year we see the pendulum swinging the other way with more participation across the board.

Today, we’ll unpack that viewpoint a bit and cover why macro drivers signal a broadening rally in 2024.

AND we’ll zero in on a couple of lagging groups in 2023 to overweight this year.

For starters, let’s address the current situation. Stocks are off to a choppy start in 2024 as investors question how quickly the Fed will cut rates.

Ignore the noise. Watch inflation.

While prices won’t necessarily fall in a straight line as the year-over-year comps get tougher, we’re confident inflation is headed lower.

Stocks look ahead.

As long as the Fed’s next move is a cut, stocks will do fine. Rate cut timing isn’t important. It’s the trend that counts.

Given the easing setup, you’ll need to cast a wider net to outperform, instead of putting all your eggs in the tech basket.

That doesn’t mean abandoning tech. It just means overweighting some of 2023’s unloved sectors too.

Macro Drivers Signal a Broadening Rally in 2024

Back when big tech was driving most of the market’s gains, the bears worried how narrow leadership meant the bull market’s days were numbered.

We said, not so fast.

Last July, we debunked that tale by proving that narrow market leadership was actually bullish. Fast forward a few months, and we’ve witnessed an extreme risk-on environment.

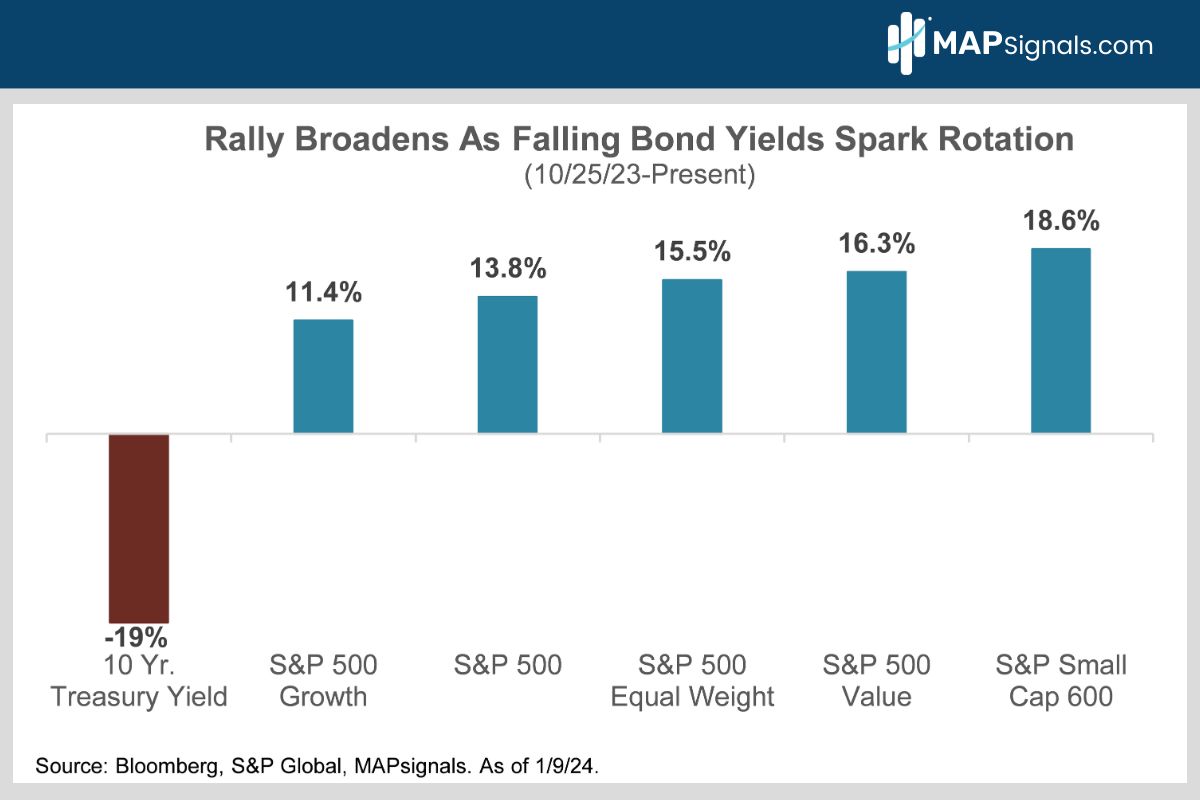

Since interest rates peaked in late October, stocks have ripped higher. This is the biggest macro data point causing the rally to broaden out.

Long-shunned, value and small-cap stocks have outperformed growth stocks while the equal weight S&P 500 has outpaced its tech-heavy, market cap weighted cousin (chart).

It’s no coincidence stocks started rallying just as Treasury yields began falling last fall. Lower rates cut the cost of doing business. They’re good for margins and corporate profits.

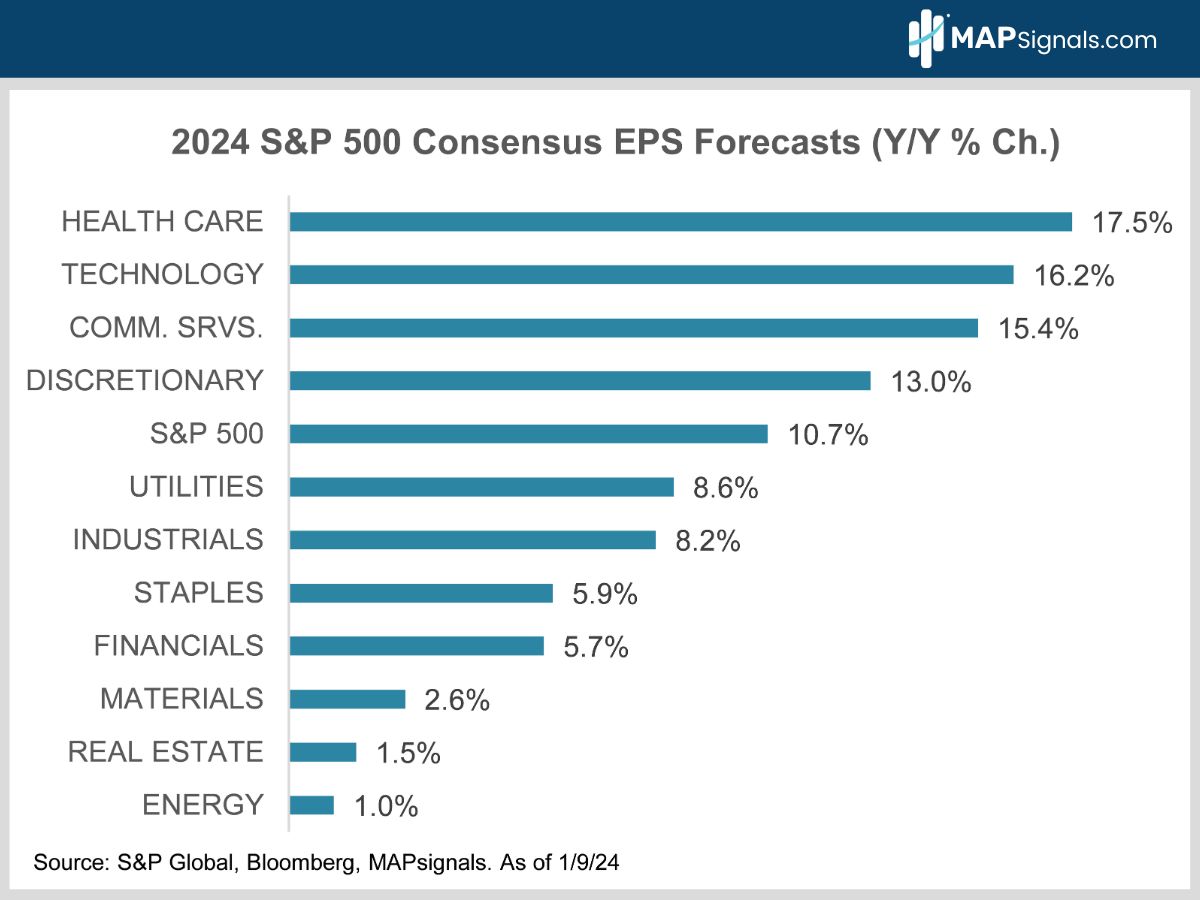

Speaking of profits, the bottom-up, sell-side analyst consensus forecasts 10.7% year-over-year S&P 500 earnings growth in 2024.

Sounds pretty healthy, right?

The problem is skepticism abounds. Strategists and buy-side fund managers think consensus numbers are too high. That’s the biggest reason they’re only lukewarm on stocks. Wall Street consensus believes the S&P finishes 2024 at 4800.

We disagree. Lower rates aren’t the only reason to be optimistic about corporate profits. We’re finding plenty of other earnings-friendly, macro signals out there.

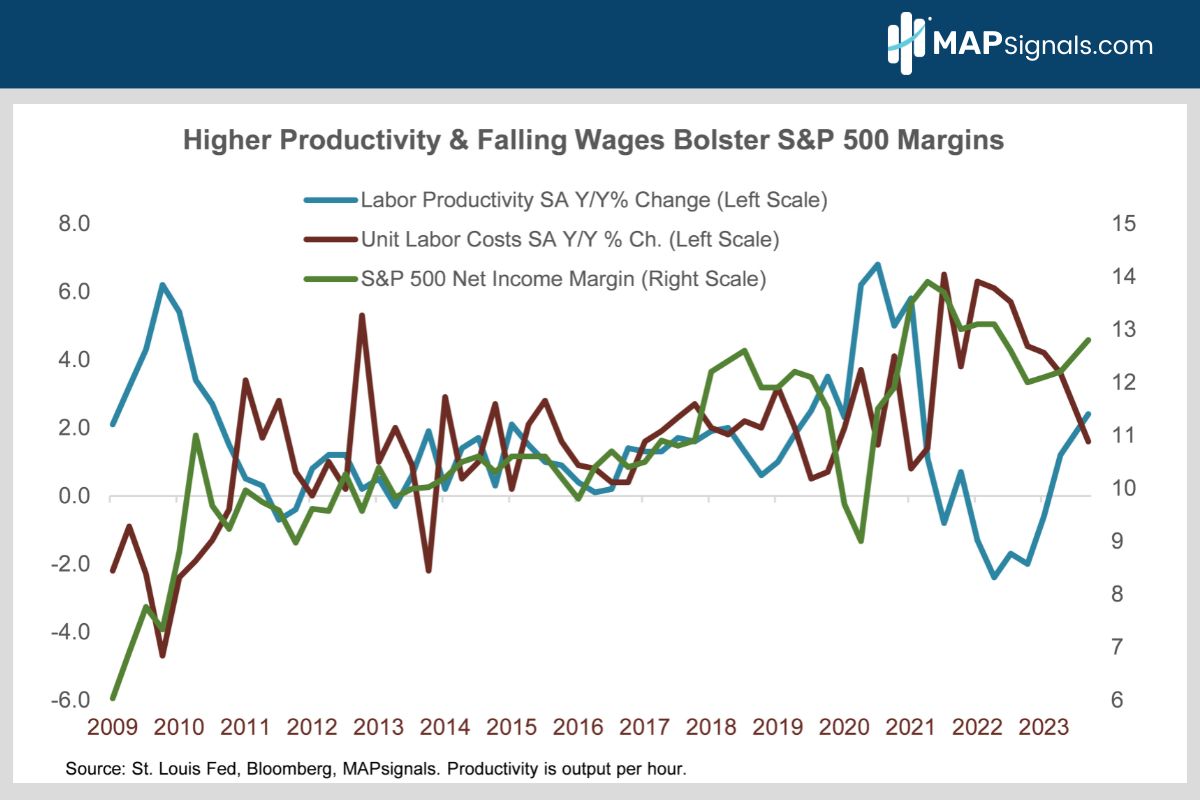

Check out this chart.

Worker productivity (output per hour) has rebounded sharply to 2.4% year-over-year growth from a negative 2.4% reading in April 2022. That’s one of the sharpest rebounds since 1950.

Meanwhile, unit labor cost (think wages) growth is down to 1.6% from its 6% peak in early 2022.

All this has helped S&P 500 net margins (what’s left after all costs and taxes) expand to 12.8% from only 12% in late 2022.

We expect to hear more good news as Q4 earnings season kicks off this week:

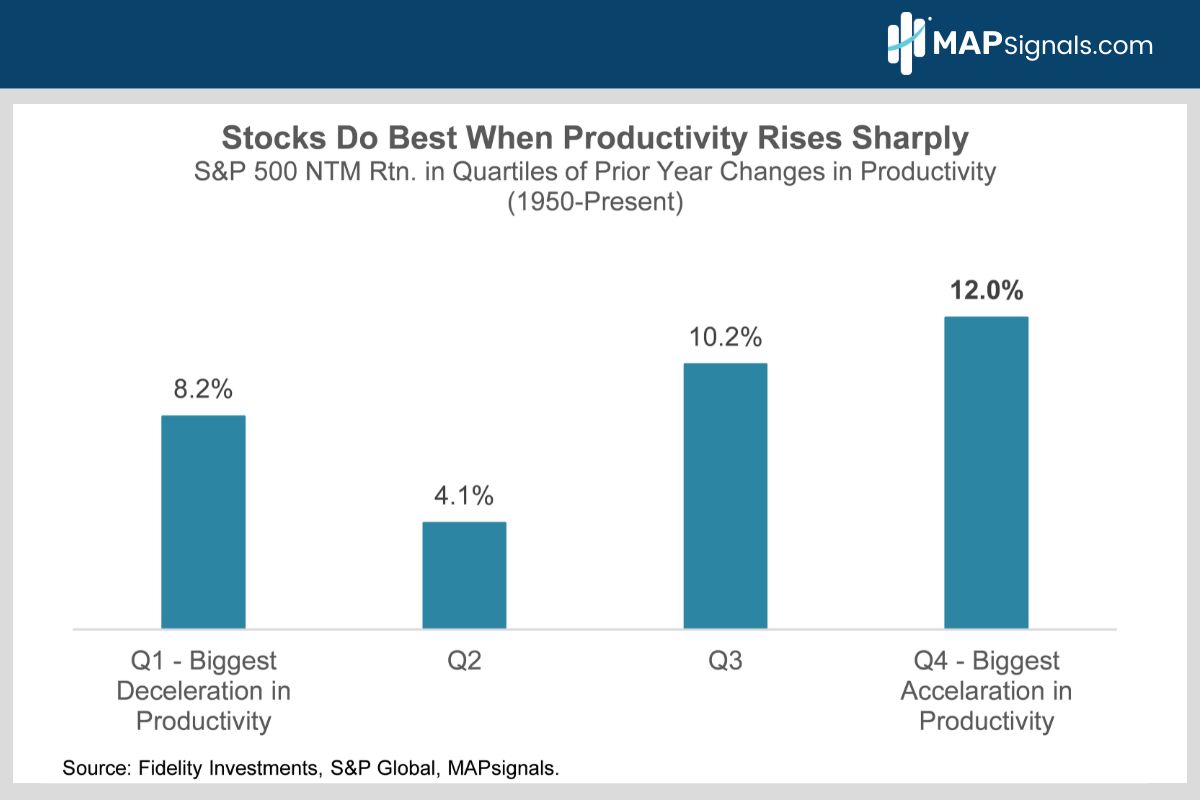

Here’s the best part. Stocks do best when productivity accelerates sharply. Since 1950, when productivity is up big, the S&P 500 rises an average of 12% in the following 12 months:

Higher productivity should trickle down to more areas of the market, further building the case for new leadership and a broadening of the rally.

Here’s how you can take advantage of this setup.

How to Play it

We rode the tech train hard last year and we still think technology will do fine on the back of a superior earnings outlook (chart) and persistent institutional buying. Tech is currently our 3rd highest ranked sector.

But with the rally finally broadening out, two of 2023’s biggest laggards – health care and financials – finally look set to lead.

Health care is forecasted to post 17.5% earnings growth this year – the highest of any S&P sector. It trades at a 12-month forward PE of only 18.5X giving it a P/E to growth ratio of about 1 – the lowest of the S&P’s 11 sectors.

Regulatory worries really held health care back in 2023. The website Predict It forecasts a toss-up Presidential election with Trump and Biden both with a 40% chance of winning the White House. Even though a Trump presidency is far from certain, the prospect of a GOP win is bullish for medical stocks.

As for financials, the sector’s 5.7% consensus estimated 2024 EPS growth forecast is likely too low. As the Fed cuts rates, short-term bond yields will fall, steepening the yield curve.

Banks borrow short and lend long so a steeper yield curve makes their loans more profitable. It boosts banks’ net interest margins.

The sector is also the 2nd cheapest in the market with a 14.7X 12MF PE.

Below shows the 2024 expected EPS growth forecast for all sectors. Health care towers above all:

OK, let’s check out how these two sectors look from a money flow perspective.

Health Care has jumped up to the top of our sector leaderboard as Big Money buying accelerates. Financials have moved up to the #2 spot:

Need more reasons to like health care stocks? You can check out last week’s writeup too.

But why stop there?

Here’s one more reason to like health care and financials.

Since 1994, they’re the two best performing sectors in the 12 months following the last Fed rate hike. Financials have averaged a 30% gain while health care has gained 29%.

The last Fed rate increase this cycle was in July. Financials and health care are only up 12% and 10% over the past six months so history says there’s plenty of upside left:

Bringing It All Together

Stocks are off to a choppy start in 2024 as investors question how quickly the Fed will cut rates.

While prices won’t necessarily fall in a straight line, we’re confident inflation is headed lower in 2024.

The Fed will have no choice but to cut rates. As long as that happens, stocks will do just fine.

Meanwhile, corporate earnings continue to be underestimated amid surging productivity and falling wage growth.

Add it all up and the macro is better than you think.

2023 was an either-or year. Tech worked much better than everything else.

Alpha will come from many places this year. As the bull market broadens out, we expect health care and financials to join tech in outperforming.

Overweight all three.

So, there you have it. The macro and earnings outlooks are better than you think, and increasing breadth means tech isn’t the only game in town anymore.

If you want our favorite health care and financial stocks we like for 2024, earlier this month we sent out a MAP PRO update highlighting 5 stocks in each group to own this year.

If you’re Financial Advisor or an RIA looking to outperform in 2024, get started with a MAPsignals PRO subscription. It’ll get you access to our portal that updates every morning, showcasing our proprietary money flow indicators and the stocks getting bought and their scores.

Market action isn’t random. It’s much easier navigating with a MAP!

Invest well,

-Alec