High Interest Rates Won’t Kill the Equity Rally

The market’s latest top macro worry is rising long-term interest rates. We’ve seen this movie before.

10-year Treasury yields recently hit 4.8%, their highest since peaking at 5% back in October 2023.

Back then, we told you to Disregard the Rate Scare and Buy Stocks Now. The S&P 500 is up 40% to 6100 since we published that report on October 9, 2023, when the index sat at 4335.

Today’s note echoes that piece: High interest rates won’t kill the equity rally.

Below, we’ll debunk the latest interest rate scare and show you why stocks don’t need falling 10-year yields to rise. We’ll include two fresh, underappreciated bullish macro drivers that signal more upside ahead.

Finally, we’ll wrap up by underscoring which sectors to overweight to unlock alpha as this bull keeps on charging.

High Interest Rates Won’t Kill the Equity Rally

Bearish talking-heads rumble on about how stocks can’t rise when 10-year Treasury yields are climbing. They cite the double whammy of higher rates drawing capital away from equities, while also raising the cost of doing business.

Sounds logical but it’s always risky to base your market view exclusively on one indicator.

Lots of other things like the economy and earnings matter too. If those are performing well while rates are rising, they may negate any negative equity impact from higher yields… allowing stocks and rates to rise together.

Let’s stress test the conventional wisdom about stocks and yields.

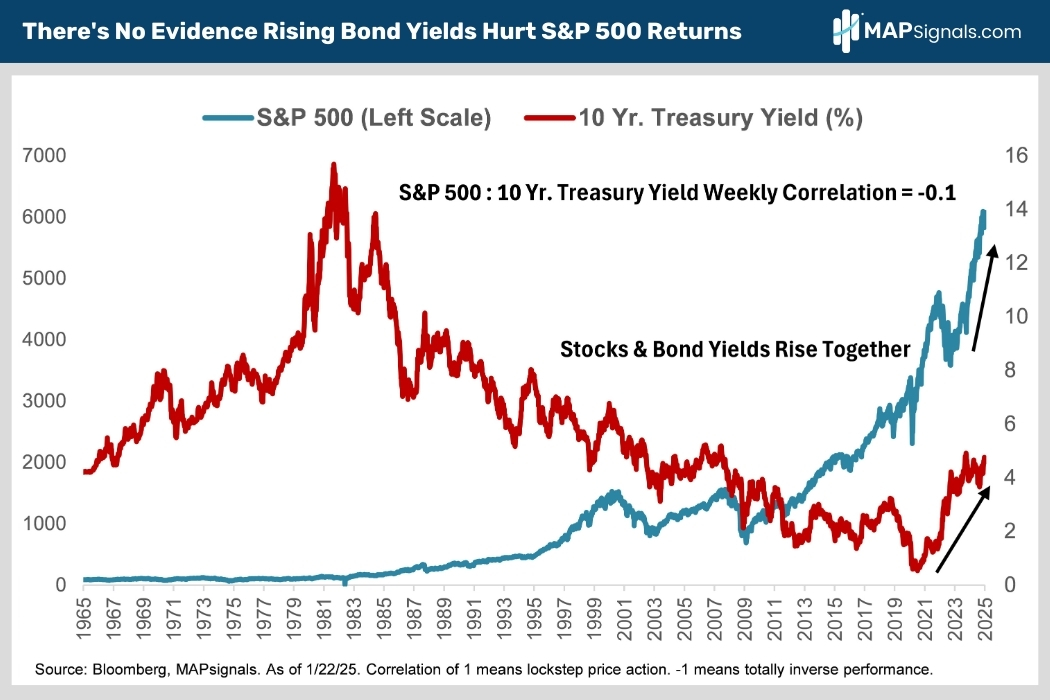

Since 1965, the correlation between the 10-year Treasury yield and the S&P 500 is -0.1%. It basically rounds to zero. Over the long run, there’s no statistical relationship between moves in the S&P 500 and the direction of 10-year bond yields (chart).

The past 5 years have been a case in point. 10-year Treasury yields bottomed in 2020 at 0.5% and have been trending higher ever since. Meanwhile, the S&P 500 has doubled since then, rising from 3000 to over 6000.

The fact that 10-year Treasury yields and the S&P have both risen sharply together since 2020 proves that stocks don’t need falling 10-year Treasury yields to do very well.

OK let’s check in on a different bond market indicator that’s more worthy of equity investors’ attention.

Tight Credit Spreads are Bullish for Stocks

Credit spreads refer to the premium companies pay above Treasury yields to borrow money.

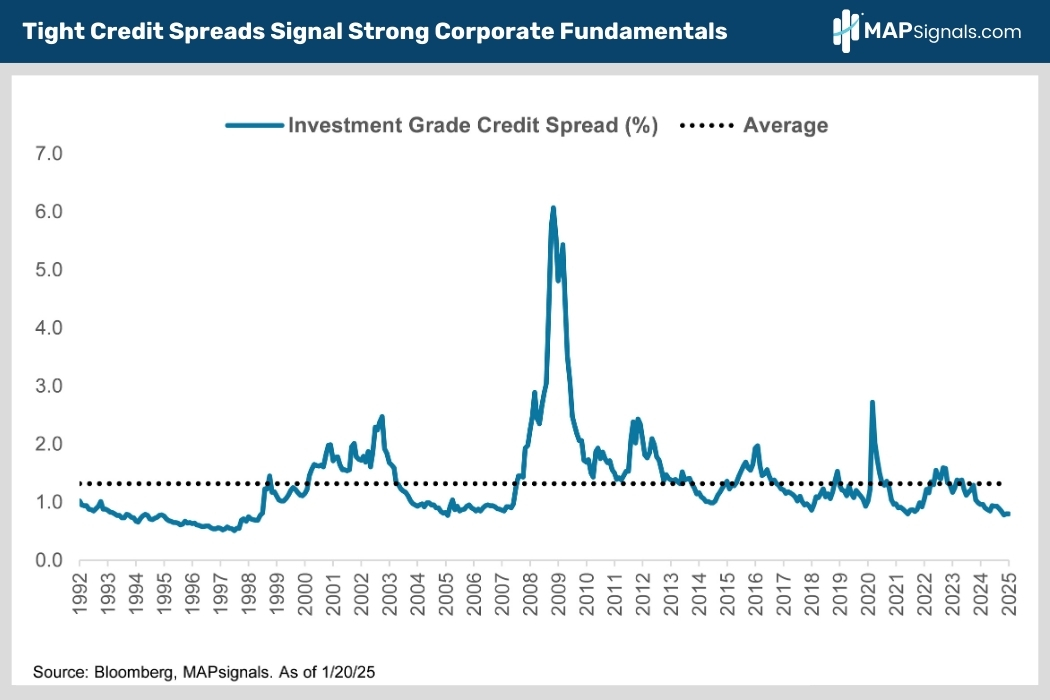

Let’s observe current investment grade credit spreads. This metric tells us what high quality names like Apple (AAPL) or JP Morgan (JPM) are paying to borrow money above what Uncle Sam pays.

Spreads are currently near record-tight levels at only 80 basis points above comparable Treasuries. That’s well below the long-term average of 132 basis points (chart).

With 10-year Treasury yields at 4.6%, blue chips only pay about 5.4% to issue 10-year corporate bonds right now.

Tight spreads help insulate blue chips from rising interest rates. This helps explain why stocks and long-term bond yields often rise together.

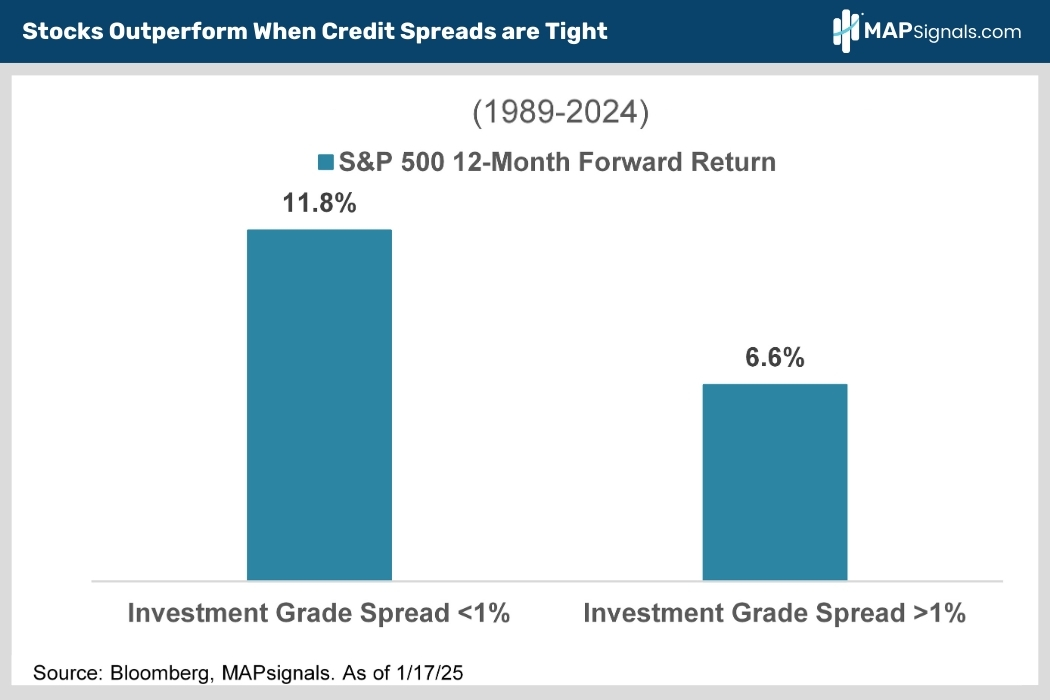

Here’s the best part. Stocks outperform when credit spreads are below 1%. This makes sense because super tight spreads reflect bond investors’ high confidence in the health of corporate America.

Since 1989, the S&P 500 has gained 11.8% in the 12-months following sub 1% investment grade credit spread readings vs. only 6.6% average advances when credit spreads have been above 1% (chart).

Even better, stocks have been less volatile in sub 1% investment grade credit spread regimes. Since 1989, the biggest S&P 500 drawdown was only 20% vs. a maximum drawdown of 69% when spreads were north of 1%.

OK let’s shift gears and check in on investor sentiment. Can it tell us where stocks are headed next?

Investor Sentiment Turns Bearish

Here’s a formula to memorize: Bull markets are born on despair, mature on skepticism, bloom on optimism, and finally die on euphoria.

While we may have finally transitioned from skepticism to cautious optimism, the latest investor sentiment survey proves euphoria is quite a way off.

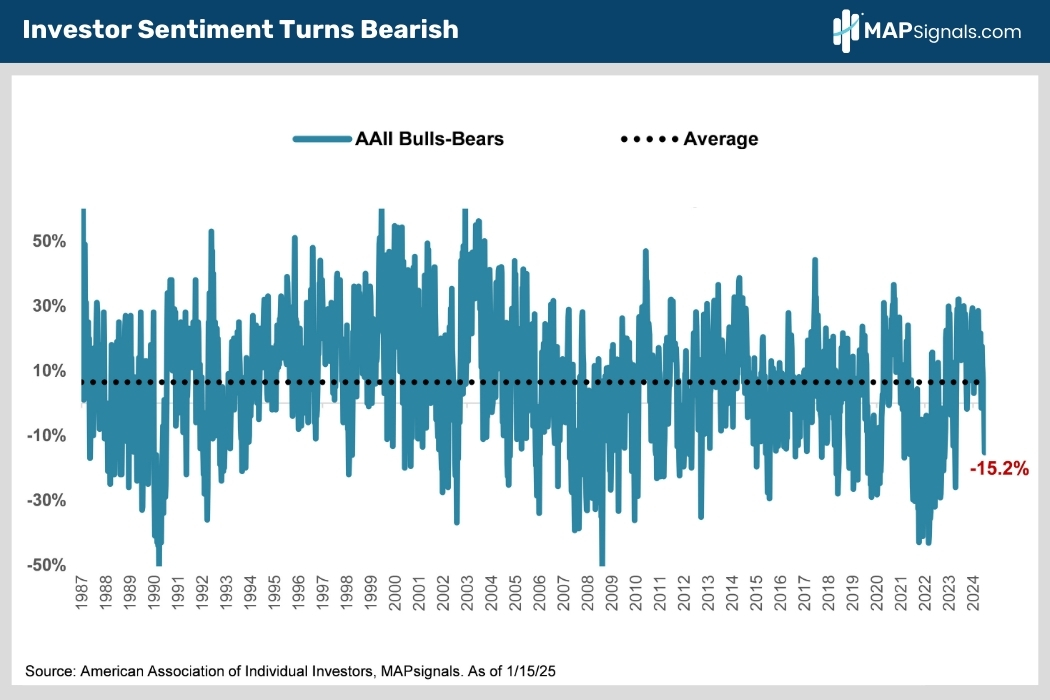

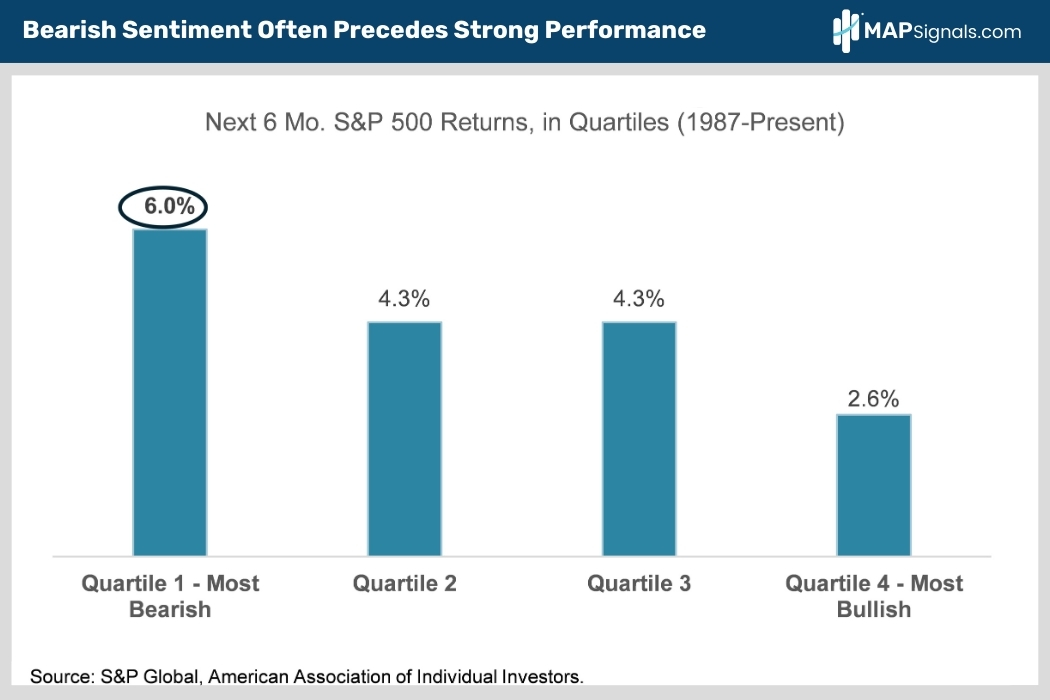

The American Association of Individual Investors (AAII) surveys its 2 million members to see how they’re feeling about stocks. We track bullish minus bearish sentiment readings. It’s averaged 6.5% since 1987.

The latest reading has bears outnumbering bulls by 15%, a bottom quartile reading since the late 80s:

Next time someone yells signs of froth are here, show them this chart!

Here’s why this is important today. The S&P 500 averages an impressive 6% gain in the 6-months following bottom quartile investor sentiment readings like we’re seeing now (chart).

All other quartiles underperform:

How to Tilt Your Portfolio

Now let’s transition to portfolio construction incorporating all these macro tailwinds.

Our 2025 outlook highlighted our preference for cyclical sectors across the market cap spectrum. Think SMID, not just large-caps. We think that’s where you’ll need to be to win big again in 2025.