2025 Outlook: Look Outside S&P 500 to Unlock Big Gains

2024 stunned just about everyone.

In rare fashion, the S&P 500 is set to post a total return of over 25% for the second year in a row. But before we discuss the future, it’s important to step back.

Two years ago, we were bold to suggest stocks can be a good bet in 2023. Recession fears dominated the tape. We didn’t buy into that narrative.

One year ago, Wall Street strategists predicted just 1% upside with the S&P 500 forecast to end 2024 at 4800.

MAPsignals took the over on that call in A Dozen Charts Signal Big Gains in 2024. Fast forward 12 months and the S&P sits above 6000, up 28% including dividends.

The party isn’t over. But investors will have to dig deeper than the S&P 500 to keep earning 20% returns.

Today, we’ll make the case for another good year for stocks. That said, the setup favors more cyclical bets deeper down the market cap spectrum.

This deep dive unpacks 10 hard-hitting bullish macro signals spanning interest rates, tariffs, valuations, earnings and more.

We’ll even debunk several popular bearish views that the media continues to push.

Altogether, these insights will lay the foundation for outperformance into 2025 and beyond.

Grab a coffee.

Then hug a bear…they’ll need it.

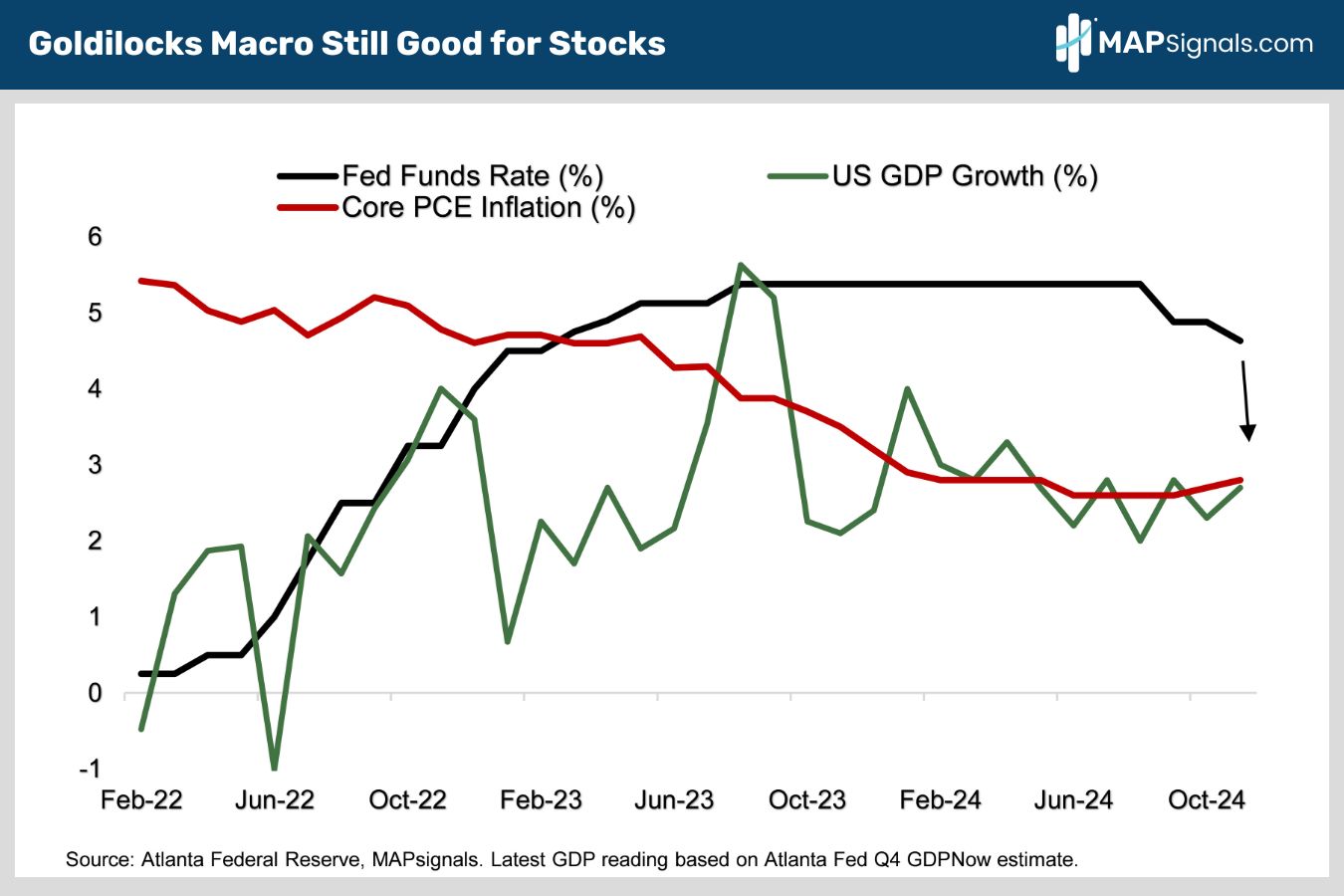

Don’t Fight a Fed That’s Cutting Rates

Media talking heads love to opine on the path of interest rates.

As we see it, there’s no recession in sight.

The much doubted, soft-landing is playing out beautifully. GDP growth remains steady at 2.7%.

A solid job market and record housing and stock appreciation continue to underpin resilient consumer spending, which represents 70% of US economic activity.

Meanwhile, core PCE inflation is down to 2.8%, with headline PCE at just 2.3%. This frees the Fed to keep cutting rates (chart 1).

Rising rates grounded stocks in 2022. It only makes sense that lower rates will stimulate equity prices:

Now let’s tackle another buzzword flashing lately: Tariffs.

Sounds scary right? Not so fast.

Tariffs Lead to Talks Which Lead to Deals

Strong growth and uncertainty over the inflationary impact of Trump’s tariff and immigration policies has markets pricing in more gradual Fed easing.

Fed funds futures expect just three more quarter point rate cuts by the end of next year, bringing the funds rate down to 3.875% from 4.625% today.

We think the Fed may cut much more than consensus expects, sparking stocks’ next leg higher.

Here’s why:

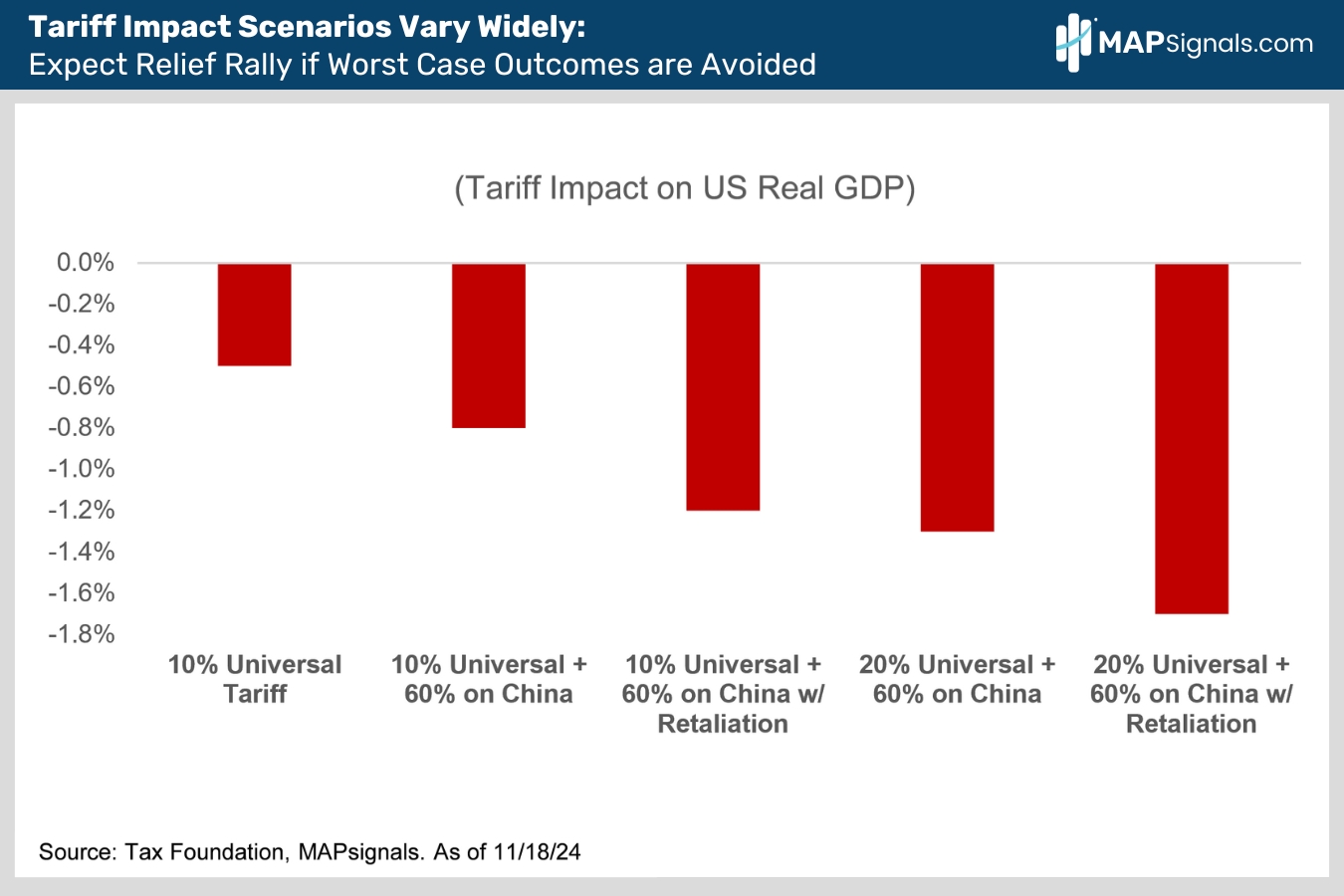

Ignore all the tariff doom and gloom. Memorize this formula instead: Tariffs > Talks > Deal.

Trump’s tariff bluster is likely just a negotiating ploy on the way to economic policies that are milder than feared. That’s exactly what transpired in Trump’s first term.

Markets don’t need risk-free conditions. They move on the gap between expectations and reality. Outcomes that are merely better than feared are all stocks need to keep rallying.

The market’s biggest pain point could surprise to the upside, sparking a relief rally.

Below are 5 potential tariff regimes and their potential GDP impact. Note the huge range between the worst- and best-case scenarios.

We expect worst case outcomes will be avoided, teeing up a relief rally.

Now, let’s do something enjoyable by debunking one of the biggest fictions on Wall Street.

Rising 10-Year Yields Aren’t Bearish for Stocks

10-year Treasury yields have risen sharply since the Fed’s first rate cut on September 18. One of the popular bear tales being spread around is that this makes stocks less attractive for a couple of reasons.

Let’s debunk them one at a time.

First off, the bears argue that rising 10-year Treasury yields reflect growing structural deficit worries in the wake of Trump’s election.

Further, the red wave means lower taxes and more debt, while tariffs and immigrant deportations will be inflationary.

Add it all up and the bond market “vigilantes” will demand to be paid higher interest rates to hold US government debt. The sky’s the limit on how high 10-year bond yields can rise.

They cry how higher rates are a double whammy for equities, representing more competition for stocks while also increasing the cost of doing business.

Sounds logical, right?

Let’s dig deeper.

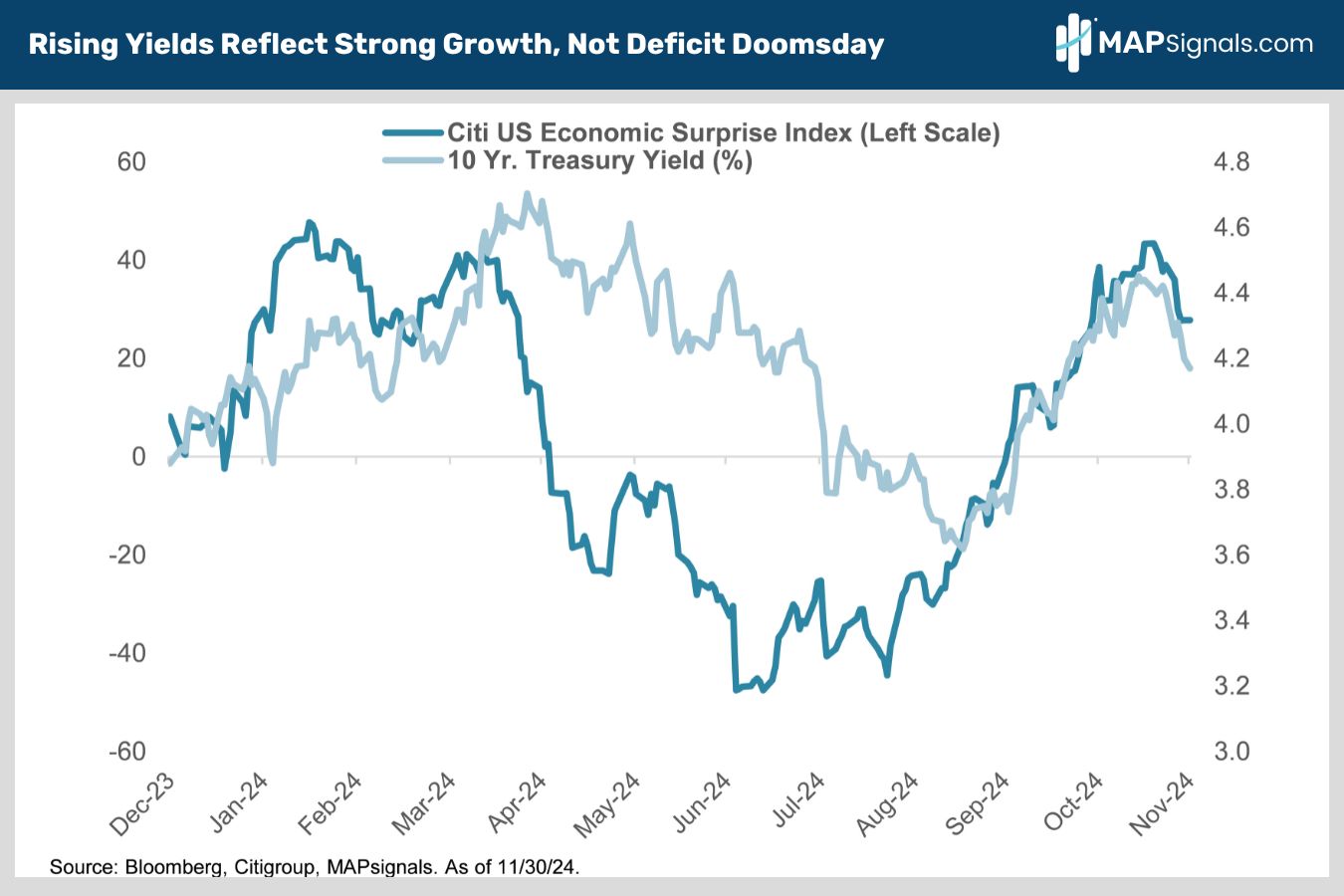

It turns out the recent rise in bond yields primarily reflects better-than-expected economic growth, which is good news for stocks.

Rising 10-year Treasury yields have mirrored the rise in the Citi Economic Surprise Index, which measures how much economic data is beating or missing consensus Wall Street forecasts.

Check out this next chart. The two data sets have moved in virtual lockstep over the past couple of months:

OK so rising yields aren’t a sign of an imminent buyers strike in the Treasury market.

Let’s move on and tackle the other big bearish narrative around rising long-term rates.

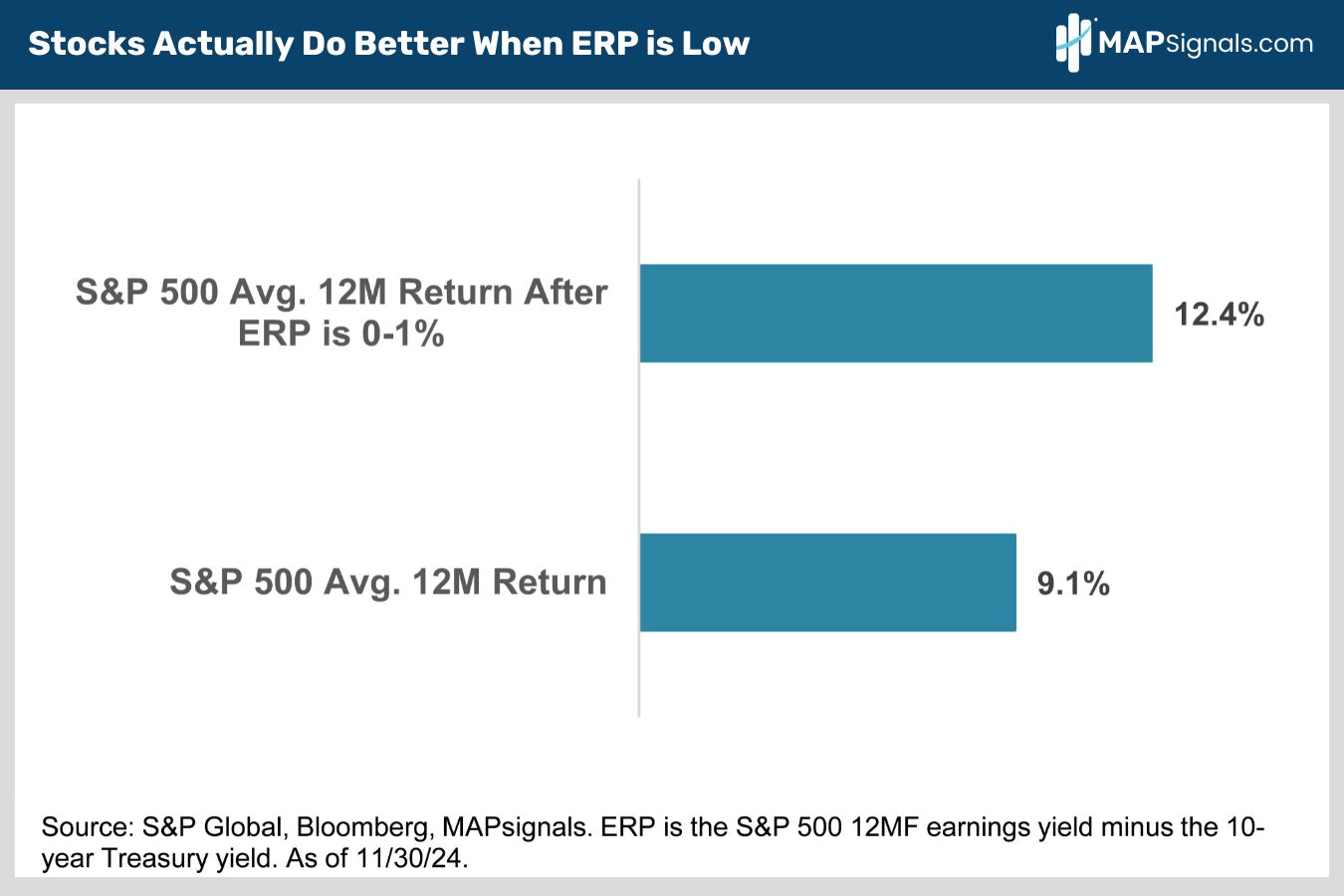

The spread between S&P 500 earnings yield (index level divided by 12-month forward S&P 500 EPS) and the 10-year Treasury yield is called the equity risk premium.

Right now, the equity risk premium (ERP) is only 0.3%. That’s the gap between the S&P 500’s 12-month forward earnings yield of 4.5% and the 10-year Treasury yield of 4.2%.

Historically, the equity risk premium has averaged 3%. The bears argue a low ERP is a sign stocks are too expensive and a bad bet relative to bonds.

Seems reasonable until you test the thesis.

Here’s what the bears miss. History shows that when the S&P 500’s equity risk premium is between zero and 1%, as it is now, the average gain over the next year is an above average 12.4% (chart).

Compared to the average 12-month return of 9.1%, lower ERP is a buy signal…not the other way around:

If you’re feeling bad for the bears now, we don’t blame you. But the bullish evidence doesn’t stop here.

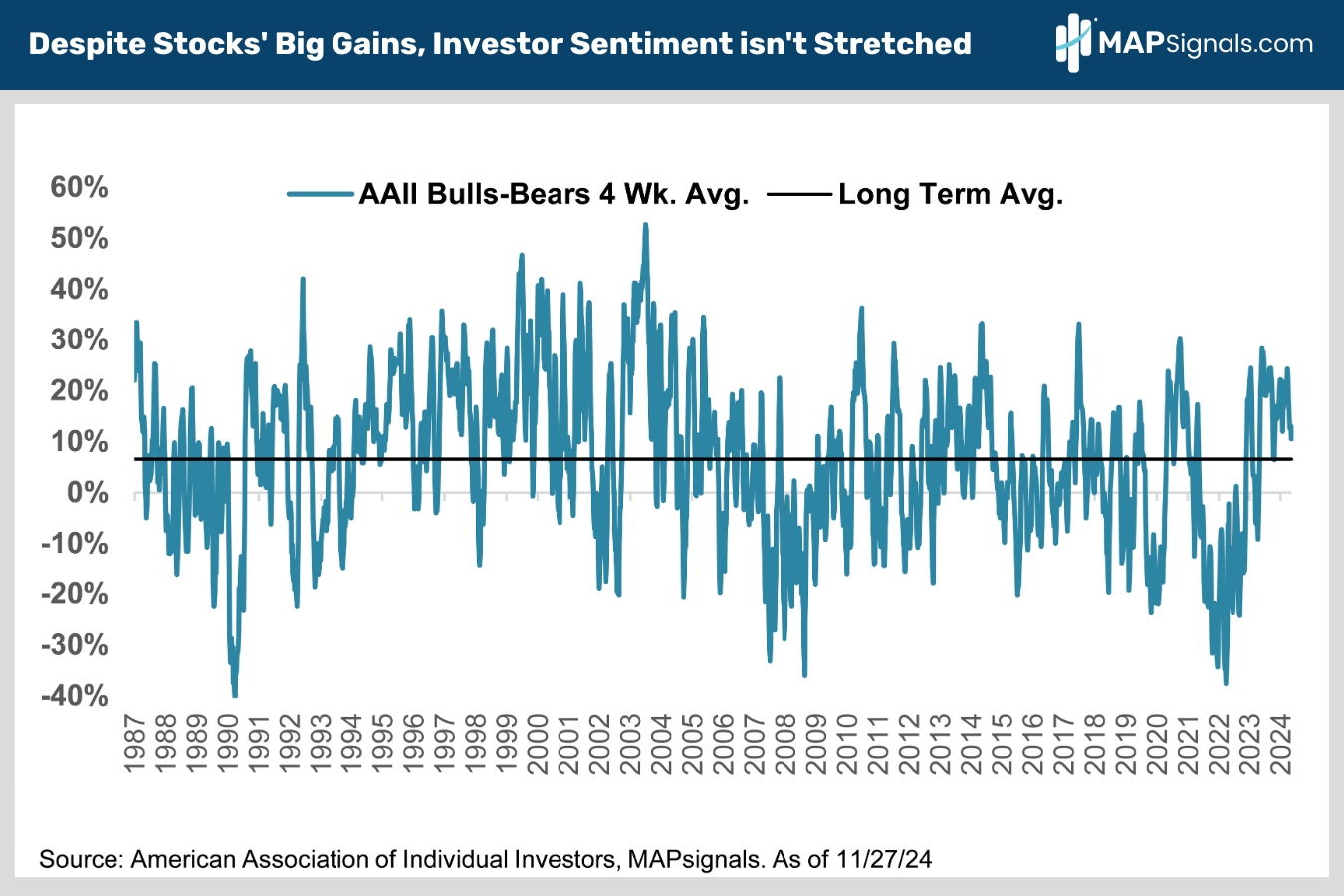

Investor Sentiment is Far from Frothy

Bull markets are born on despair, mature on skepticism, bloom on optimism, and finally die on euphoria.

While we may have finally transitioned from skepticism to cautious optimism, the latest investor sentiment surveys prove widespread euphoria is still a long way off.

The American Association of Individual Investors (AAII) surveys its 2 million members to see how they’re feeling about stocks.

We track the 4-week average of bullish minus bearish sentiment readings. It’s averaged 6.5% since 1987.

The latest reading has bulls outnumbering bears by 10.5 %, only slightly above average since the late 80s:

Next time someone yells signs of froth are here, show them this chart!

Now, let’s transition to portfolio construction incorporating all these bullish tailwinds.

Look Outside S&P 500 to Unlock Big Gains in 2025

Investors need to be more creative with portfolio construction in 2025.

There is a list of reasons why.

First, long-term interest rates are up roughly 12% since early September. With PCE inflation at just 2.3%, the clear takeaway from the ramp in 10-year Treasury yields is that investors expect stronger economic growth.

That’s a good thing.

Second, a red wave is fanning traders’ economic optimism. The Trump administration’s tax and regulatory regimes will be much less onerous…which should lead to a resurgence in long-subdued M&A activity.

Next, there’s the tariff situation. If they’re used surgically, don’t expect them to spike inflation and undermine Trump’s pro-business agenda.

Finally, the friendly political backdrop isn’t the only reason investors are upbeat on growth.

Remember earlier when I showed how Fed easing is a big positive for stocks? Here’s the evidence.

When the Fed isn’t rushing to cut rates to avert a recession or a crisis (Dot-Com Bubble, Great Financial Crisis, Covid-19 etc..) stocks shine.

And here is the all-important takeaway: Small- and mid-cap stocks have historically led the way.

Since 1995, the S&P 500 has gained an average of 17.6% in the 12 months after the first Fed rate cut when a recession is avoided. But mid and small-cap stocks have done much better, averaging gains of 22.9% and 25.9%, respectively (chart).

All three indexes are up less than 10% since the Fed’s September 18 initial rate cut, so history says there’s plenty of upside left through September 2025.

Let’s keep drilling down.

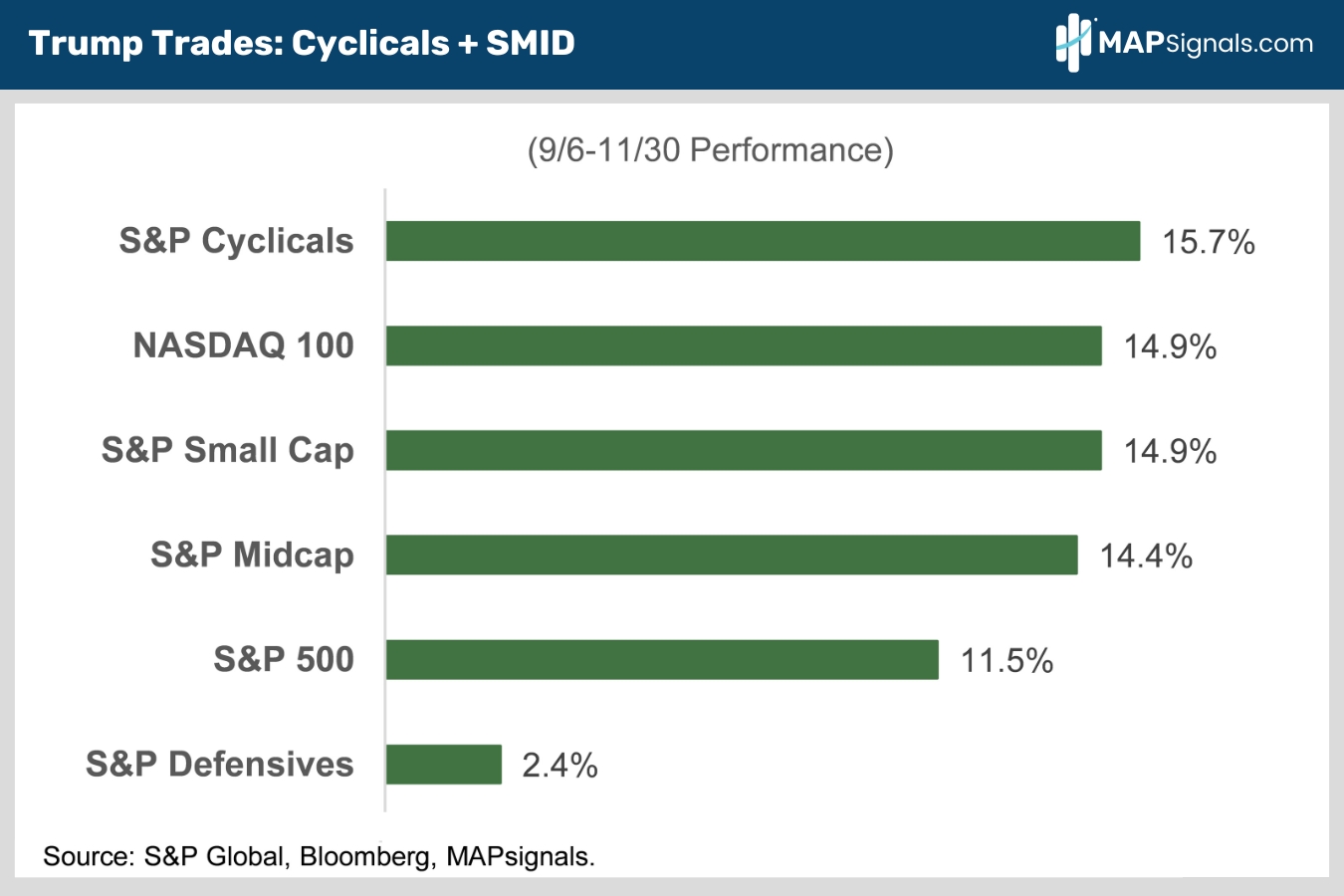

Against this optimistic macro backdrop, it’s no surprise that more economically sensitive trades like small-cap, mid-cap, and large-cap cyclicals are outperforming the broader S&P 500 while defensives lag badly (chart).

Stock picking is key in this environment.

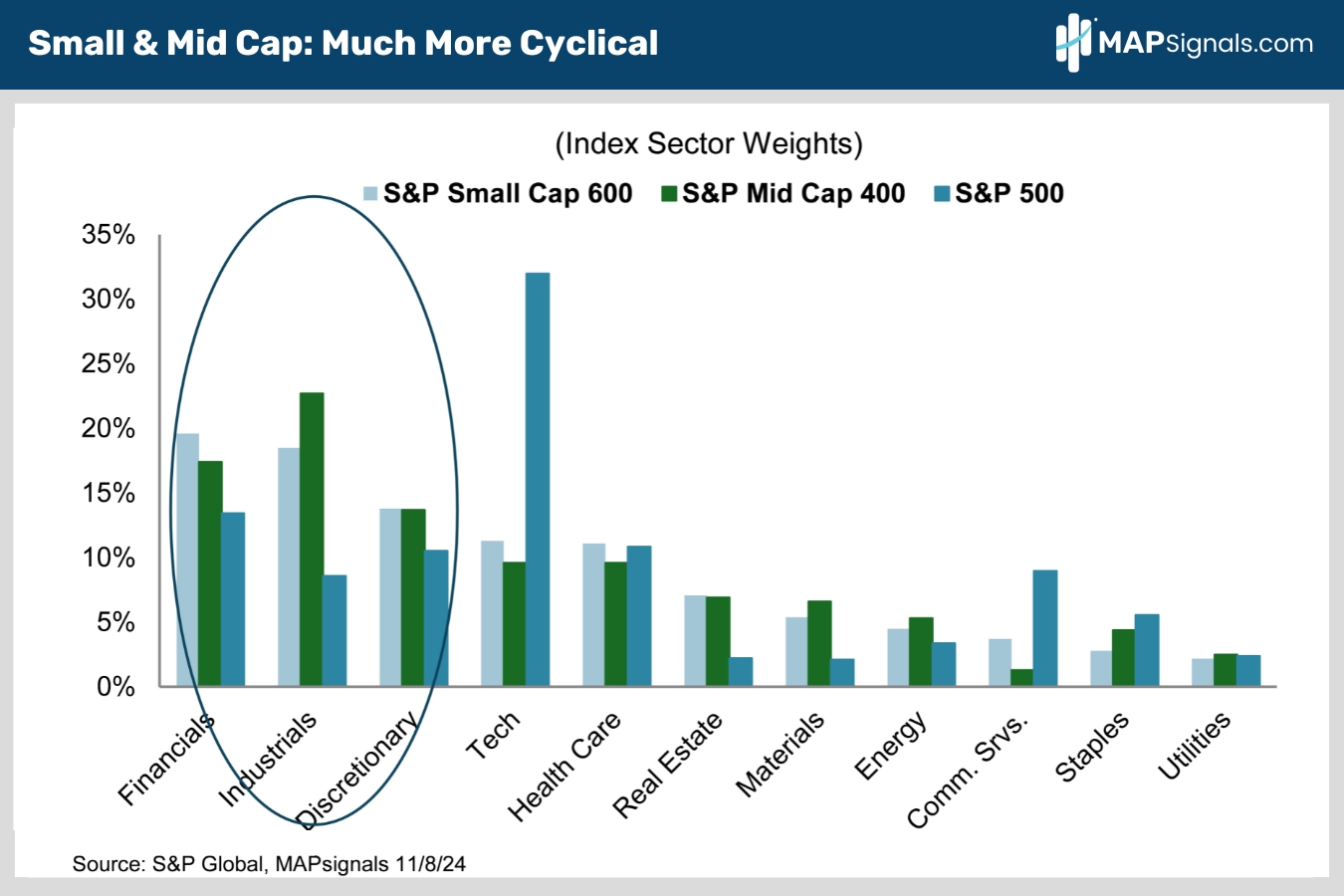

Small- and mid-caps are super-cyclical compared to the S&P 500. That’s thanks to their 52% and 54%, respectively, combined weightings to financials, industrials and discretionary vs. only 32% in the S&P (chart).

Betting smaller is making the wager on a pickup in economic activity:

Let’s not leave out the 2 other important equity drivers: earnings and valuations.

Outside of the S&P 500, opportunities abound.

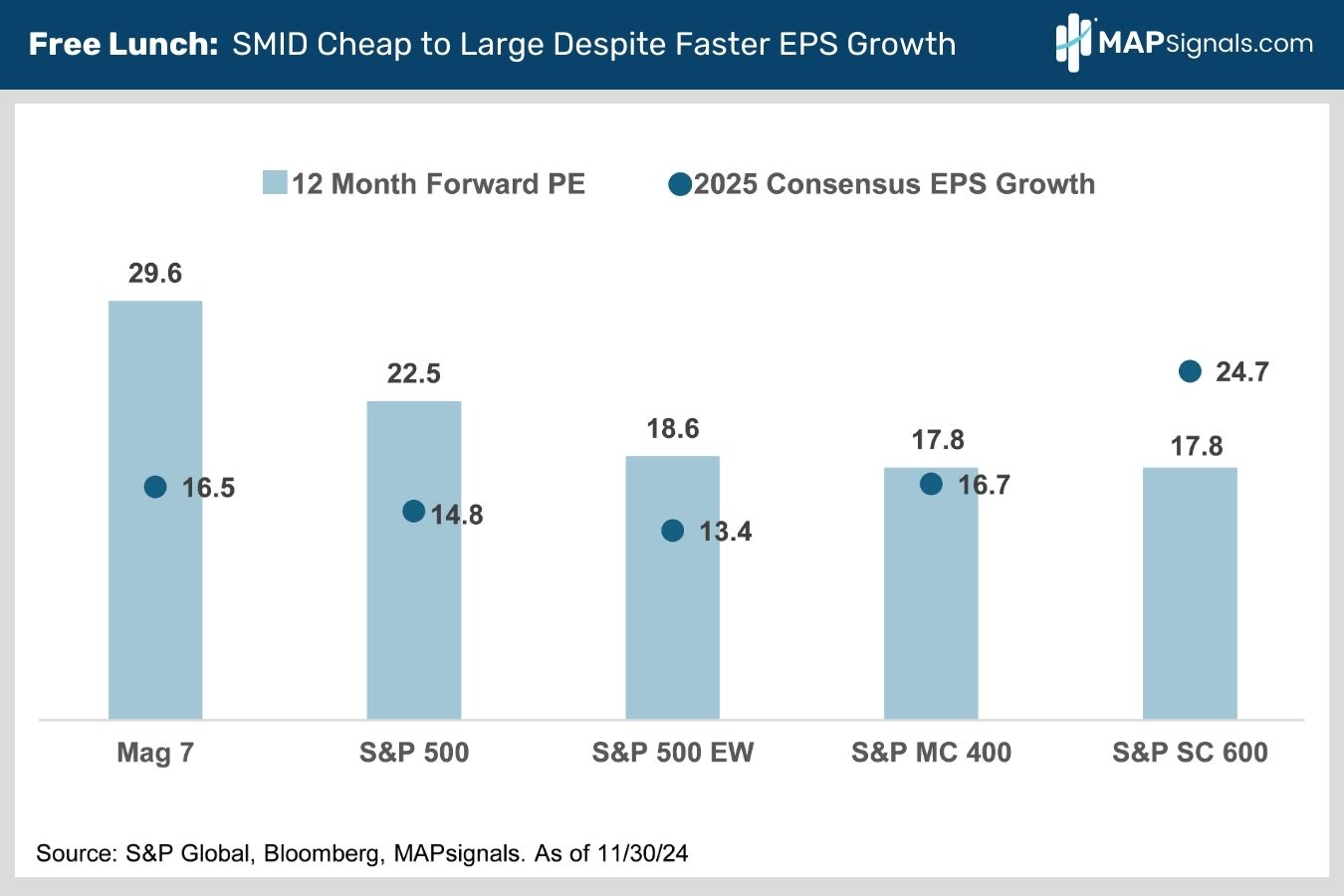

The S&P Small Cap 600 and S&P Mid Cap 400 are estimated to post 24.7% and 16.7% 2025 EPS growth, respectively, vs. just 14.8% for the S&P 500 (chart).

Before the election, confidence in those juicy forward EPS estimates was low. Economic nervousness kept investors from paying up for cyclicals and SMID stocks.

Fed easing and the red wave are giving investors increased belief that companies can hit lofty 2025 consensus earnings growth forecasts.

Cyclical sectors and small- and mid-cap indexes have the most to gain from this positive macro re-appraisal.

That’s finally unlocking higher valuations for cyclicals and SMID equities amid greater achievability of 2025 EPS forecasts.

Here’s the kicker. Despite their recent burst of outperformance and better 2025 estimated EPS growth, small- and mid-cap stocks are still very cheap to large caps, with both trading at just 17.8X 2025 EPS vs. the S&P’s 22.5X (chart).

As a result, SMID is our favorite play for 2025 as we expect the bullish re-rating to continue.

Here’s where the MAPsignals unique approach shines.

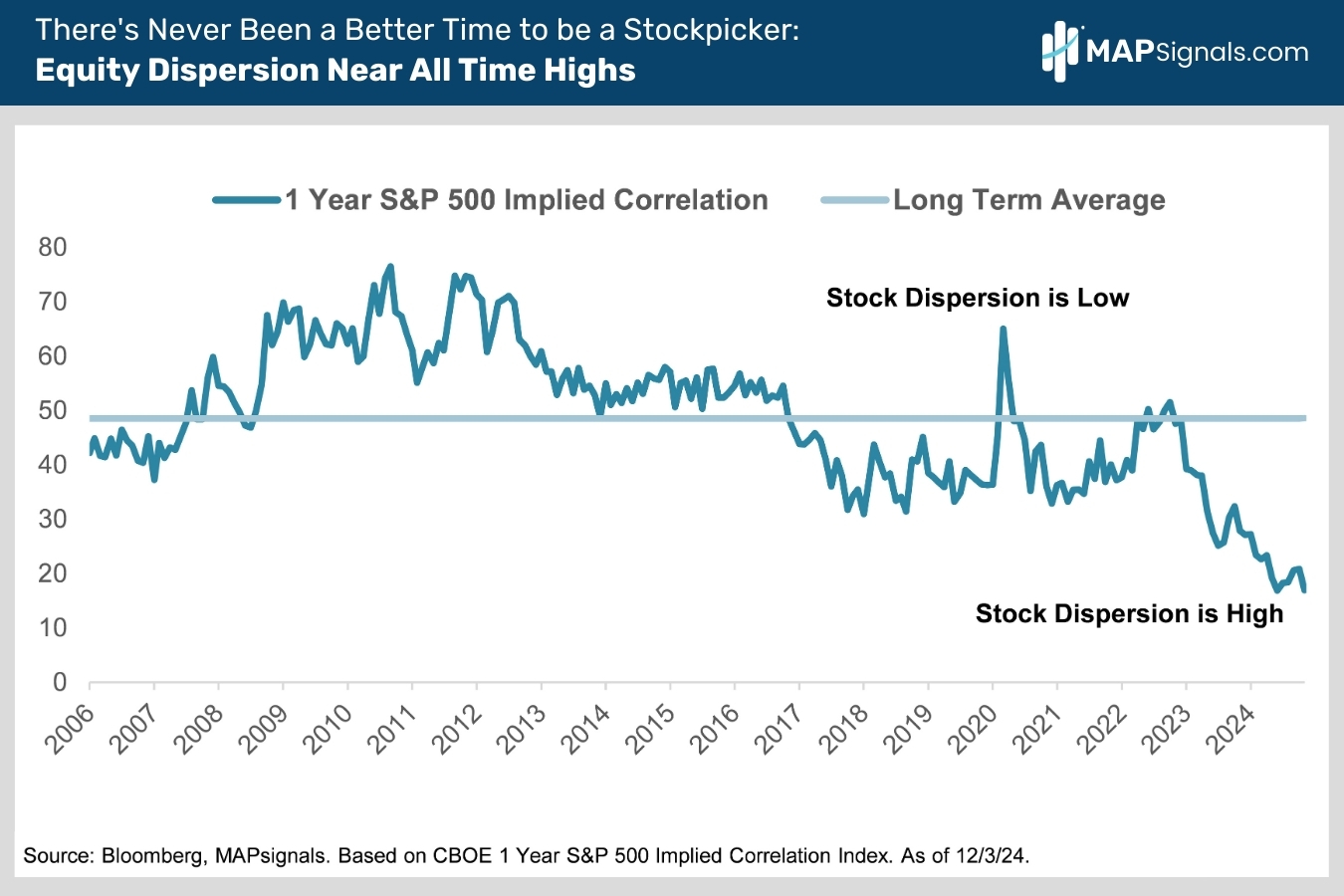

It’s a Stock Picker’s Market

We all love finding big winners. Some markets are more suited to picking individual stocks than others. The good news is there’s rarely been a better time to pick stocks than right now!

The term correlation in finance describes how one stock behaves relative to another.

When correlation is high, most stocks are moving in a similar direction at any given time.

This tends to happen when big macro events like the COVID pandemic, the surprise 2016 Trump Presidential victory, or the Great Financial Crisis are driving trading activity.

Conversely, when correlation is low, there’s a big divergence in how single stocks perform.

We tend to see this environment when the macro environment is calmer and impacting sectors differently, leaving more room for company specific trends to dominate.

…think A.I., robotics, water management, fitness & recreation, FinTech, etc.

That’s exactly what’s happening right now. Correlation is near an all-time low of only 17%. That compares to a long-term average of 48% (chart). Check it out:

You get more bang for your buck when you pick the right stocks. Fortunately for MAPsignals subscribers, we have a secret weapon to spot these mega-trends early in their growth phase: Institutional sponsorship.

After spending years on Wall Street trading desks, the backbone of the MAPsignals process revolves around spotting unusual institutional trading volumes.

That alerts us to waves of capital rushing into single stocks each and every day. When we overlay our proprietary scoring metric on top of these signals, outlier companies emerge.

Like Super Micro Computer (SMCI) in the summer of 2022. Or Celestica (CLS) in the summer of 2023.

Or more recently AppLovin (APP), first spotted in March of 2024. Since the first appearance on our Top 20 report, shares have gained 502% through 12/3/2024.

The blue bars below indicate when APP was a top-rated buy signal:

There’s a whole world of stocks on the Big Money’s radar.

You just need a map to find them!

Here’s the Bottom Line

Bull markets die on euphoria and we aren’t there yet.

While we may have finally transitioned from skepticism to cautious optimism, 2025 should be another good year for stocks.

But to keep earning 20%+, bet on large-cap cyclical sectors like financials, tech, discretionary and industrials, and the small- and mid-cap indexes that are loaded with them.

Record earnings growth beckons in 2025 with small-caps leading the way.

SMID is our favorite play as we expect 2024’s bullish re-rating to continue.

We all love finding big winners. Some markets are more suited to picking individual stocks than others. The great news is there’s rarely been a better time to pick stocks than right now!

If you want to find specific high-quality stocks beaming with Big Money support, get started with a MAPsignals PRO subscription.

It’ll get you access to our portal that updates every morning, showcasing the stocks getting bought and their scores.

MAP your own stocks and ETFs. AND you’ll get our prized Top 20 list in your inbox every Tuesday!

There are plenty of cyclical stocks poised to keep ripping in 2025. If you’re a Registered Investment Advisor (RIA) or are a serious investor, use a MAP to find them!

Invest well,

-Alec